smoother

roads ahead.

WE SEE THINGS DIFFERENTLY

HENDERSON TAYLOR

Terms of Business

This document and other associated documentation may also be available in other formats. Please contact us for further information.

Terms of Business Agreement – Personal Lines

Applying to General Insurance customers – please read this document carefully and contact us immediately if there is anything in this document that you do not understand or with which you disagree.

It sets out the terms and conditions on which we agree to act for you, contains details of our responsibilities together with your responsibilities both to us, to insurers and to other third-party providers. This is our standard client agreement upon which we intend to rely on. This “Terms of Business Agreement” (TOBA) supersedes all previous versions issued to you. Your receipt of this document constitutes your informed consent to its contents and by instructing us you are accepting this TOBA.

Company Contact Details

Premier Insurance Centre Ltd who also trade as Miller Insurance Brokers & Henderson Taylor 424/426 High Street, Winsford Cheshire CW7 2DS

01606 863 400

info@premierins.co.uk

Premier Insurance Centre Ltd is authorised and regulated by the Financial Conduct Authority (FCA) which allows us to advise on, arrange, make arrangements with a view, and assist in the administration and performance of general insurance contracts. We are also allowed to provide credit broking, debt administration and debt collection services. Our Firm Reference Number (FRN) is 306607. You can check this on the Financial Services Register by visiting the FCA’s website https://register.fca.org.uk/s/ or by telephoning the FCA on 0800 111 6768.

Contents

Definitions

About us

Our service

Limitations of our liability

Important information (consumers only)

The duty of fair presentation (commercial customers only)

Financial crime

Solvency of insurers

Terms of payment

Howweholdyourmoney

Quotations

Renewals

Mid-termtransferredbusiness

Notificationofincidents/claims

Cancellation

Remuneration,fees&charges

Complaints

Financial Services Compensation Scheme

Confidentiality&dataprotection

Communications/documentation

Terminationofourauthoritytoactonyourbehalf

Third-partyrights

General

1. Definitions

‘’Consumer’’ means anyone acting outside their trade or profession in respect of the insurance cover requested or arranged. ‘’Company’’, ‘’we’’, ‘’us’’ or ‘’our’’ means Premier Insurance Centre Ltd

‘’You’’ or ‘’your’’ means you (and/or your appointed agent).

“Statutory” means officially written down in a law. “Liable/liability” means legally responsible.

3. Our service

As an independent insurance intermediary, we generally act as the agent of our client, which means we would act on your behalf. We are subject to the law of agency, which imposes various duties on us. However, in certain circumstances we may act for and owe duties of care to other parties, including the insurer. We will advise you when these circumstances occur, so you will be aware of any conflicts of interest (situations which may affect our role as your agent).

We offer a wide range of insurance products and services which may include:

Offering you a single or range of products from which to choose a product that suits your insurance needs;

Advising you on your insurance needs;

Arranging suitable insurance cover with insurers to meet your requirements;

Helping you with any later changes to your insurance you have to make;

Providing all reasonable help with any claim you have to make.

We have access to many leading insurance companies and will advise you where we have provided advice based on a personal recommendation, which means the product is suitable for the person to whom it is made or is based on the circumstances of that person. We will also advise you when we offer you a policy on the basis of a fair and personal analysis, which means we have looked at a sufficiently large number of insurance contacts on the market to enable us to make a personal recommendation. Where we have provided advice based on a personal recommendation but not on the basis of a fair and personal analysis, we will advise you:

- If we are under a contractual obligation to conduct insurance distribution exclusively with one or more insurers (which means we are tied to use these insurers), and will provide you with a list of those insurers; or

- If we are not under a contractual obligation to conduct insurance distribution with one or more insurers and will provide you with a list of insurers with which we may and do place business.

Before the insurance contract is concluded and after we have assessed your demands and needs, we will provide you with advice and make a personal recommendation, unless we advise otherwise. This will include sufficient information such as the main features of the product’s cover, any unusual restrictions or exclusions, any significant conditions or obligations and the period of cover to enable you to make an informed decision about the policy, together with a quotation which will itemise any fees that are payable in addition to the premium. This documentation will also include a statement of your demands and needs which you should read carefully.

4. Limitations of our liability

The following provisions set out our entire financial liability to you.

You acknowledge and agree that you shall only be entitled to make a claim against us and not against any individual employee or consultant engaged by us. Our liability for losses suffered by you arising under or in connection with the provision of our services, whether in contract, tort (a civil wrong including negligence), breach of statutory duty, or otherwise (including our liability for the acts or omissions of our senior management, employees and any appointed representatives) shall be limited to £10,000.00 per claim. Any claim or series of claims arising from one act, error, omission, incident, or original cause shall be considered to be one claim. We shall not be liable to you for any loss of profit or loss of business whether directly or indirectly occurring and which arises out of or in connection with the provision of our services.

Nothing in this paragraph shall exclude or limit our liability for death or personal injury caused by our negligence or for loss by our fraud, fraudulent misrepresentation or breach of regulatory obligations owed to you. You are welcome to contact us to discuss increasing the limitations of our liability and or varying the exclusions set out above.

5. Important information (consumers only)

Under legislation, it is your duty as a consumer to take reasonable care not to make a misrepresentation to an insurer, which means you cannot provide any false information.

A failure by you to comply with the insurers request to confirm or amend details previously given is capable of being a misrepresentation. It is important that you ensure all statements you make on proposal forms, claim forms and other documents are full and accurate and we recommend that you keep a copy of all correspondence in relation to the arrangement of your insurance. An insurer has the right to take corrective measures if it can deem the misrepresentation to be either deliberate, reckless, or careless.

If in doubt about any point in relation to your duty to take reasonable care and subsequent misrepresentations, please contact us immediately.

6. The duty of fair presentation (commercial customers only)

It is your responsibility to provide a fair presentation of the insurance risk based on you conducting a reasonable search for information. This could require you to obtain information from senior managers within your organisation or other parties to which the insurance relates or who carry out outsource functions for your business.

You must disclose every material circumstance which you know or ought to know, or failing that, disclose sufficient information to put your insurer on notice that it needs to make further enquiries. You must ensure that any information you provide is correct to the best of your knowledge and representations that you make in expectation or belief must be made in good faith. If you fail to make a fair presentation of the risk, this may result in additional terms or warranties being applied from inception of the policy or any claim payment being proportionately reduced. In some cases, this could result in your policy being declared void by an insurer and your premiums returned. Any deliberate or reckless breach of the duty of fair presentation could result in your policy being declared void by an insurer with no refund of premium.

If in doubt about any point in relation to material circumstances and reasonable search, please contact us immediately.

7. Financial crime

Please be aware that current UK money laundering regulations require us to obtain adequate ‘Know Your Client’ information about you. We are also required to cross check you against The Office of Financial Sanctions Implementation (OFSI) HM Treasury consolidated list of Financial Sanctions Targets in the UK as part of the information gathering process.

We are obliged to report to the National Crime Agency and/or Serious Fraud Office any evidence or suspicion of financial crime at the first opportunity and we are prohibited from disclosing any such report. We will not permit our employees or other persons engaged by them to be either influenced or influence others in respect of undue payments or privileges from or to insurers or clients.

8. Solvency of insurers

We cannot guarantee the solvency of any insurer with which we place business. This means that you may still be liable for any premium due and not be able to recover the premium paid, whether in full or in part, should an insurer become unable to cover its own financial obligations. If you have any concerns regarding any insurer chosen to meet your insurance requirements, you should inform us as soon as possible.

9. Terms of payment

Our payment terms are as follows (unless otherwise agreed by us in writing):

New policies: immediate payment on or before the starting date of the policy.

Alterations to existing policies: immediate payment on or before the effective date of the change.

Renewals: due in full before the renewal date.

If payment is not received from you in accordance with the above terms, we, or your insurer may cancel or lapse the relevant policy/policies, which could mean that part or all of a claim may not be paid. You may also be in breach of legally required insurance cover.

If you choose to pay for your insurance premium using a finance provider, your details will be passed onto them. We will provide you with a breakdown of the costs of your monthly instalments and subsequently a document outlining key features of their credit agreement with you including any fees they apply and the cost of charges if you have failed to make a payment (default charges).

It is important that you take time to read this document and must contact us if you do not receive this. If you have any queries or questions, either about the service provided by the finance provider or their terms and conditions you should in the first instance contact them. Where your policy is paid via the finance provider and you choose to renew your cover, we will again continue to pass your details to them.

If any direct debit or other payment due in respect of any credit agreement you enter into to pay insurance premiums is not met when presented for payment, or if you end the credit agreement, we will be informed of such events by the finance provider.

In certain circumstances we may be contractually obliged by the finance provider to notify your insurer to cancel the policy. Where we are not contractually obliged to do so by the finance provider, if you do not make other arrangements with us to pay the insurance premiums you acknowledge and agree that we may, at any time after being informed of non-payment under the credit agreement, instruct on your behalf the relevant insurer to cancel the insurance and to collect any refund of premiums which may be made by the insurer and use this refund to offset the amount levied by the finance provider on us. If this amount is not sufficient to cover all our costs, we reserve the right to pursue any additional debt owed to us through a due legal process. You will be responsible for paying any time on risk charge and putting in place any alternative insurance and/or payment arrangements you need.

Upon receiving your strict acceptance to pay for insurance premiums through the finance provider, we will instruct them to proceed with your application for credit. This process will involve the provider searching public information that a credit reference agency holds about you and any previous payment history you have with that provider. The credit reference agency will add details of your search and your application to their record about you whether or not your application is successful.

Please read carefully the pre-contractual explanations and the information regarding the cost of credit (including any representative examples). Together they provide important information in relation to the credit facility available from the finance provider. Credit is available subject to status.

10. How we hold your money

All client money is handled by us. Client money is money that we receive and hold on behalf of our clients during the course of our dealings such as premium payments, premium refunds, and claim payments. This money will be held by us either as agent of the insurer or agent of the client, determined by the agreement we have in place with each insurer. Where money is held as agent of the insurer, this means that when we have received your cleared premium, it is deemed to have been paid to the insurer.

Our standard accounting practice is to take our commission upon receipt of your cleared funds prior to payment of the premium to the insurer.

The FCA requires all client monies, including yours, to be held in a trust account, the purpose of which is to protect you in the event of our financial failure since, in such circumstances; our general creditors would not be able to make claims on client money as it will not form part of our assets.

We hold all client monies with one or more approved banks, as defined by the FCA, in a Statutory Trust bank account in accordance with the FCA client money rules. Under these arrangements, we assume responsibility for such monies and are permitted to, and may:

For the purpose of effecting a transaction on your behalf, pass your money to another intermediary, including those resident outside the UK who would therefore be subject to different legal and regulatory regimes. In the event of a failure of the intermediary, this money may be treated in a different manner from that which would apply if the money were held by an intermediary in the UK. Please inform us if you do not agree to this.

Retain for our own use, any interest earned on client money.

Unless we receive your written instruction to the contrary, we shall treat receipt of payment from you and of any claim payment and/or refund of premium which fall due to you, as being with your informed consent to the payment of those monies into the Statutory Trust bank account.

11. Quotations

Unless otherwise agreed, any quotation given will normally remain valid for a period of 30 days from the date it is provided to you.

We reserve the right to withdraw or amend a quotation in certain circumstances, for example, where the insurer has altered their premium/terms for the insurance since the quotation was given, where there has been a change in the original risk information/material circumstances disclosed, or if a claim/incident has occurred since the terms were offered.

12. Renewals

You will be provided with renewal terms in good time before expiry of the policy, or notified that renewal is not being invited.

Unless you advise otherwise, renewals are invited on the basis that there have been no changes in the risk or cover required, other than those specifically notified to us or your insurers (see section 5 ‘Important information’ and section 6 ‘The duty of fair presentation’).

It is very important that you check the information provided at renewal to confirm it remains accurate and complete. If any of the information is incorrect or if your circumstances have changed, you should contact us immediately so we can update your details.

13. Mid-term transferred business

When we are appointed to service insurance policies other than at their inception or renewal and which were originally arranged via another party, we shall not be liable during the current insurance period for any loss arising from any errors or omissions or gaps in your insurance cover or advice not supplied by us.

Should you have any concerns in respect of a policy, which has been transferred to us, or if you require an immediate review of your insurance arrangements, you must notify us immediately. Otherwise, we shall review your insurance arrangements and advise accordingly as each policy falls due for renewal.

14. Notification of incidents/claims

Your policy documentation will provide you with details on who to contact to make a claim. It is essential to notify immediately all incidents that may result in a claim against your insurance policy. You must do so whether you believe you are liable or not.

Any letter or claim received by you must be passed on immediately, without acknowledgement. Only by providing prompt notification of incidents can your insurance company take steps to protect your interests.

Claims payment will be made in favour of you. If you require a payment to be made to a third party, then you must confirm the required payee name and details and provide a brief explanation for your request.

Please contact us for guidance on claiming under your policy.

15. Cancellation

Your policy document will detail your rights to cancel your insurance once you have taken it out. Depending on the type of policy you have purchased, you may be entitled to cancel within 14 or 30 days of either conclusion of the contract or receiving your policy documentation, whichever occurs later. This is often referred to as a cooling off period.

Where you cancel a policy before renewal, you will be responsible for paying a charge to meet the cost of cover provided and administration expenses – please see section 16 ‘Remuneration, fees & charges’. To enable your insurer to process the cancellation, you will need to return certificates and any official documents to our office within 30 days of your notice to cancel.

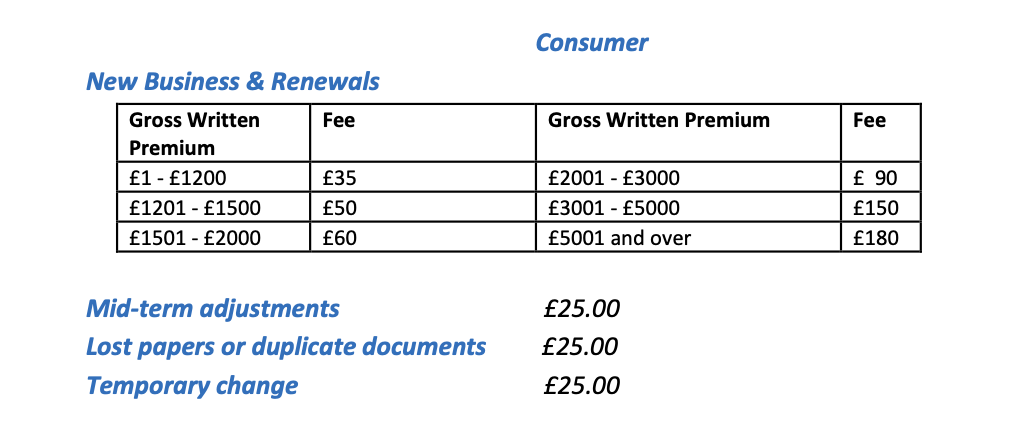

16. Remuneration, fees & charges

In most cases we are paid by commission from the insurer, but in some circumstances, we may charge you a fee instead of commission or a combination of both, in which case this will be confirmed to you in writing at the time of incepting or renewing your policy.

Our fees will be confirmed to you clearly and in writing at the time of incepting or renewing your policy and will always be disclosed to you before you commit to purchasing the product. There may also be occasions when an additional fee is sought, for example changes to the risk that required significant further advice and placement of additional coverage or substantial involvement in any large, difficult, or complex claims.

In addition, we also make charges as detailed below to cover the administration of your insurance. Any applicable insurance premium tax will be shown on the documentation we provide to you. These fees are non-refundable.

We may occasionally receive additional remuneration from insurers, claims management providers and others.

Where you choose to pay your premium by instalments, we may use a scheme operated by your insurer, or we may use a single finance provider. Where we arrange premium finance on your behalf, we are remunerated for our assistance in putting this financing in place by way of commission. We will advise you of any commission payable by the finance provider in relation to a credit agreement where knowledge of the existence or amount of commission could affect our impartiality in recommending a particular product or that may have a material impact on your transactional decision.

You are entitled at any time to request further information regarding the amount of any remuneration which we may have received as a result of placing or renewing your insurance cover. To the extent that this is not possible for an amount to be given, we will provide the basis for its calculation.

Where a policy is cancelled before renewal, insurers charge to cover their costs, with the balance refunded to you, subject to no claim having been made. Full details will be available in your policy. In the event of an adjustment giving rise to a return of premium, the amount may be refunded or held to credit.

Your attention is specifically drawn to the following:

Where you cancel your policy after the expiry of the cooling off period or where you request a mid-term adjustment which results in a refund of premium, we reserve the right to charge you for our time and costs. This will usually result in us reducing the amount refunded to you by the FULL amount of the commission and fees we would have received had you not cancelled. However, any charge made will not exceed the cost of the commission and fees we would have earned. For certain commercial insurance policies, insurers will only provide cover where the premium is due in full on inception of the policy. This means that no refund will be paid if the policy is cancelled before renewal. We will advise you if this affects you. Bank details may be retained for the purposes of refunds and claims payments that may be made by BACS (Bankers Automated Clearing System).

17. Complaints

It is our intention to provide you with the highest possible level of customer service at all times. However, we recognise that things can go wrong occasionally and if this occurs, we are committed to resolving matters promptly and fairly.

Should you wish to complain you may do so:

• In writing to the Complaints Manager Karl Holland

• By telephone on 01606 863 400

• By e-mail at karl@premierins.co.uk

• In person by visiting our office (see above for address)

Should you not be satisfied with our final response, you may be entitled to refer the matter to the Financial Ombudsman Service (FOS). More information is available on request or on their website https://www.financial-ombudsman.org.uk. Further details will be supplied at the time of responding to your complaint.

18. Financial Services Compensation Scheme (FSCS)

We are covered by the Financial Services Compensation Scheme, and you may be entitled to compensation from the scheme depending on the type of business and circumstances of the claim if we cannot meet our obligations. Further information about compensation scheme arrangements is available from the Financial Services Compensation Scheme website at https://www.fscs.org.uk.

19. Confidentiality and data protection

We are a data controller for the information you provide to us including individual, identification and financial details, policy history and special category data (such as medical or criminal history).

Details of our legal basis for processing your information, along with details of any third party recipient whom it may be necessary to share your personal data with in order to fulfil the contract, retention period for data held, security of your data, your rights under the UK General Data Protection Regulations (UK GDPR) including the right to complain can be found in our full ‘Privacy Notice’ on our website at www.premierins.co.uk.

20. Communications/documentation

21. Termination of our authority to act on your behalf

You or we may terminate our authority to act on your behalf by providing at least 14 days’ notice in writing (or such other period we agree). Termination is without prejudice to any transactions already initiated by you, which will be completed according to these Terms of Business unless we agree otherwise in writing.

You will remain liable to pay for any transactions or adjustments effective prior to termination, and we shall be entitled to retain any and all commission and/or fees payable in relation to insurance cover placed by us prior to the date of written termination.

22. Third party rights

Unless otherwise agreed between us in writing, no term of this Terms of Business is enforceable by any third parties.

23. General

If any provision of these Terms is found to be invalid or unenforceable in whole or in part, the validity of the other provisions of these Terms and the remainder of the provision in question will not be affected.

These Terms shall be governed by the laws of England and Wales and the parties agree herewith that any dispute arising out of it shall be subject to the exclusive jurisdiction of the relevant court.

These Terms supersede all proposals, prior discussions, and representations (whether oral or written) between us relating to our appointment as your agent in connection with the arranging and administration of your insurance.

These Terms constitute an offer by us to act on your behalf in the arranging and administration of your insurance.

In the absence of any specific acceptance communicated to us by you (whether verbal or written), you are deemed to accept our offer to act for you on the basis of these Terms, by conduct, upon you instructing us to arrange, renew or otherwise act for you in connection with insurance matters.

We will issue all documentation to you in a timely manner. Documentation relating to your insurance will confirm the basis of the cover and provide details of the relevant insurers. It is therefore important that the documentation is kept in a safe place, as you may need to refer to it or need it to make a claim.

A new policy/policy booklet is not necessarily provided each year, although a duplicate can be provided at any time upon request.

You should always check the documentation to ensure all the details are correct and if this is not the case, you should contact us immediately. If documents are issued by electronic means or via an internet portal, paper documents are available free of charge on request.